Understanding the Changing Tax Landscape Current Tax Benefits: A Favorable Position Double cab pickups are the backbone of the construction…

Understanding the Changing Tax Landscape Current Tax Benefits: A Favorable Position Double cab pickups are the backbone of the construction…

Navigating HMRC Time to Pay Arrangements: A Lifeline for UK Businesses In the complex world of business finance, one of…

We’re back with another blog post and this time we’re diving into a topic that isn’t everyone’s cup of tea…

Last week, as part of the mini-budget, the government began announcing help for small businesses. This blog gives you the…

Back in his Spring Statement in March of 2022, then Chancellor Rishi Sunak announced significant changes to National Insurance. The…

Ask HMRC to verify you had a new child which affected your eligibility for the self-employed income support scheme. If…

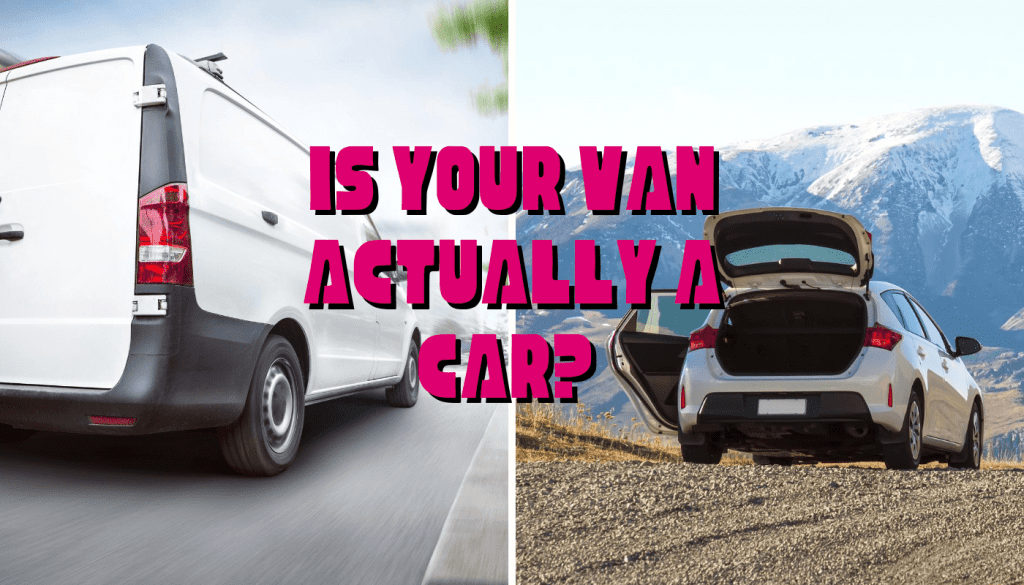

“Should I buy a car or a van” is a question we frequently get asked at 1 Accounts. Our recommendation…

Business Bounce Back Loans – what are they and should you apply for one? Since the scheme launched in May…

The help and advice that is available from the Government is forever changing. This is the latest update we have…

Capital Gains rules are changing! If you are a property investor or “accidental” landlord this is the blog for you….

Quick Links

Contact Details

Privacy Policy | Cookie Policy | © 2026 Copyright 1 Accounts | All Rights Reserved | Company number – 7385792